SMM reported on July 3:

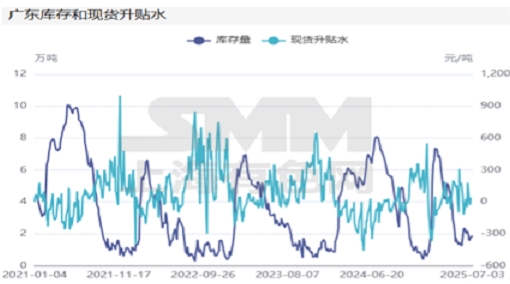

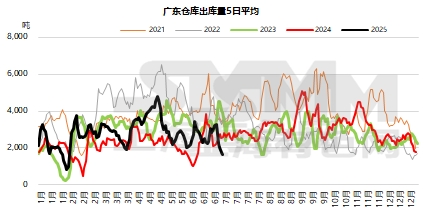

Guangdong region: This week, premiums and discounts in the region initially jumped and then pulled back. At the beginning of the week, as suppliers had already cleared their inventory last week, they chose not to lower prices for shipments but instead refused to budge on prices. However, as copper prices continued to rise, downstream purchasing sentiment declined, forcing suppliers to lower prices for shipments. By Thursday, high-quality copper was quoted at a premium of 100 yuan/mt, unchanged from last Thursday. Standard-quality copper was quoted at a premium of 30 yuan/mt, up 20 yuan/mt from last Thursday. SX-EW copper was quoted at a discount of 20 yuan/mt, also up 20 yuan/mt from last Thursday. On Thursday, the price spread between premiums and discounts for standard-quality copper in Shanghai and Guangdong was 40 yuan/mt higher in Shanghai, indicating a relatively small spread with no room for cross-regional cargo transfers. According to SMM statistics, as of Thursday, the total inventory in Guangdong warehouses was 18,700 mt, an increase of 1,200 mt from last Thursday. The combined warrants were 6,300 mt, an increase of 2,200 mt from last Thursday. Specifically: This week, warehouse arrivals were 9,200 mt/week, a significant decrease of 5,100 mt/week from last week, far below the annual average (14,000 mt/week). Both imported and domestically produced copper arrivals decreased significantly this week. Outflows from warehouses were 8,100 mt/week, a decrease of 8,000 mt/week from last week, far below the annual average (14,200 mt/week). With copper prices rising sharply, end-users had a strong wait-and-see sentiment and only made small purchases, leading to a sharp decline in outflows from warehouses this week.

Looking ahead to next week, from what we understand, both imported and domestically produced copper arrivals will remain limited. Moreover, many processing enterprises have indicated that due to the impact of high copper prices, they will reduce their capacity utilization rates. Therefore, we believe that next week will see a situation of tighter supply and even weaker demand, with weekly inventory expected to increase slightly, but the increase will not be significant.

》Subscribe to view SMM metal spot historical prices